Long/short rations is an excellent indicator for overall market sentiment. The bar chart below indicates that +58% (updated every 15-mins) of the market is/or has been bearish the EUR and there lies the danger after this early morning Greek deal announcement.

The potential risk of a Greek default is subsiding after EU Policy makers agreed a bailout for the country. Investors will be more than willing to ‘load up’ again on risky assets. However, the speculative market remains very short of the EUR and as recently as last week, Macro Hedge Funds were again accumulating EUR short positions for a break lower outright. Obviously, after this morning’s early agreement, this looks less likely now that the Greek deal has brought a couple of months’ worth of stability to the Euro-zone debt markets. Improved sentiment along with stronger than expected US data could see the pair challenge a new year high print.

Thus far, the market has “brought the rumor sold the factâ€Â. EUR has rallied +0.8% in the O/N session on reports that the Euro-group has agreed on a new financing package for Greece, but has dropped from its high of 1.3293. Most of the other G10 currencies have managed to pair some of their original gains. The Market will now wait to see what North America wants to do.

The Euro-group have agreed to +EUR130b Greek rescue package. The key details include:

- The new package is expected to bring Greece’s debt to GDP ratio down to +120.5% in 2020.

- The haircut for PSI will be raised to +53.5% or more from +50%. The agreement would pave the way for the PSI offer to begin today or tomorrow

- Prospective profits and accrued interest on ECB ownership of Greek bonds will be used as an official contribution to reduction of Greek debt, albeit with this action taken by individual euro area governments after an ECB distribution of these.

- Greece is to pass a constitutional amendment giving debt service payments priority over other budgetary expenditure

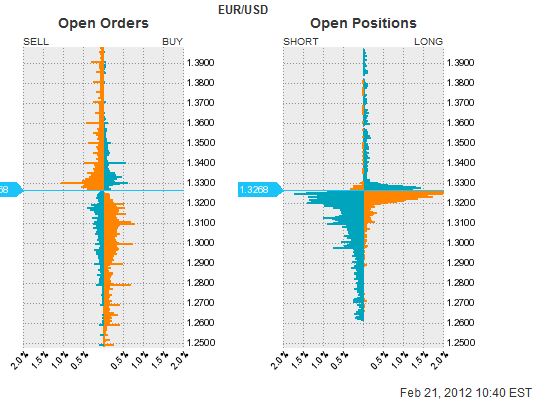

The direction of the EUR likely depends on the shift to the PSI process and the likely need for non-voluntary participation and the strength of this participation. As you can see from our Order Positions, the market for some time has been trading under water, continually selling upticks, obviously trying to improve their off-side average.

With the Greek deal only being inked earlier this morning, the market has very little opportunity to change sentiment. To date, market sentiment has been rather negative towards a constructive Greek deal. Position graphs have the investors selling into a ‘positive’ outcome all the way up from 1.29 to current levels (1.3236). However, with the lack of a sell off on an inked deal, the bears will begin to question how long they can afford to finance these short EUR positions. Market positing has bears on the verge of closing out this short EUR chased/lemming trades. From the Open Order Graphs there are very little intraday order sentiments being expressed. Investors are willing to closing watch market moves and deal with exit accordingly, ‘heart over mind’!

Now that a deal is done, market can expect larger ranges and greater volatility. Until now, investors and dealers had been hoping for more market movement to solidify investment strategies, lack of market movement can be attributed to the lack of market convictions. With the EUR pricing getting away from the dominant positioned bears, the market can expect further losses short term and a EUR currency threatening to trade at year highs before a market reprieve. This should back volatility and larger ranges!

Market price action during the North American Open indicates that the Greek debt agreement, intended to avoid a disorderly default, seems to have been priced into the market last week. Continuing worries about the fragility of the bailout package is again allowing investors to move towards the safe haven of the ‘dollar.’ With Global factors continuing to trump domestic data, lack of confidence and risk taking, will find it tough going for the market to print new highs, and pressurize the weaker shorts. The market again lack conviction on open while digesting the immediate outcome.

Investors will now be looking hard at the PSI (Private Sector Involvement) and the non-voluntarily participation rate for direction. It would seem that the market will be content to continually sell EUR rallies until otherwise convinced not to do so!

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019