Futures Higher But Pull-Back May Not Be Over

US equity markets are on course to bounce back from their blip on Thursday, with futures around a third of a percentage point higher, slightly shy of the gains seen in Europe and Asia.

Wednesday’s sell-off suggested that investors had lost a little faith in the two month long rally that saw indices make new record highs almost every day. While they still look vulnerable to a small pull-back, it would appear investors are not quite ready to concede yet. Stocks have come off another strong earnings season and with Trump’s tax reform plan running into difficulties in Congress, it seems investors are using the opportunity to lock in some profit.

DAX Moves Higher as Cyclicals Rebound

UK Retail Sales Beat Expectations But Worrying Trend Continues

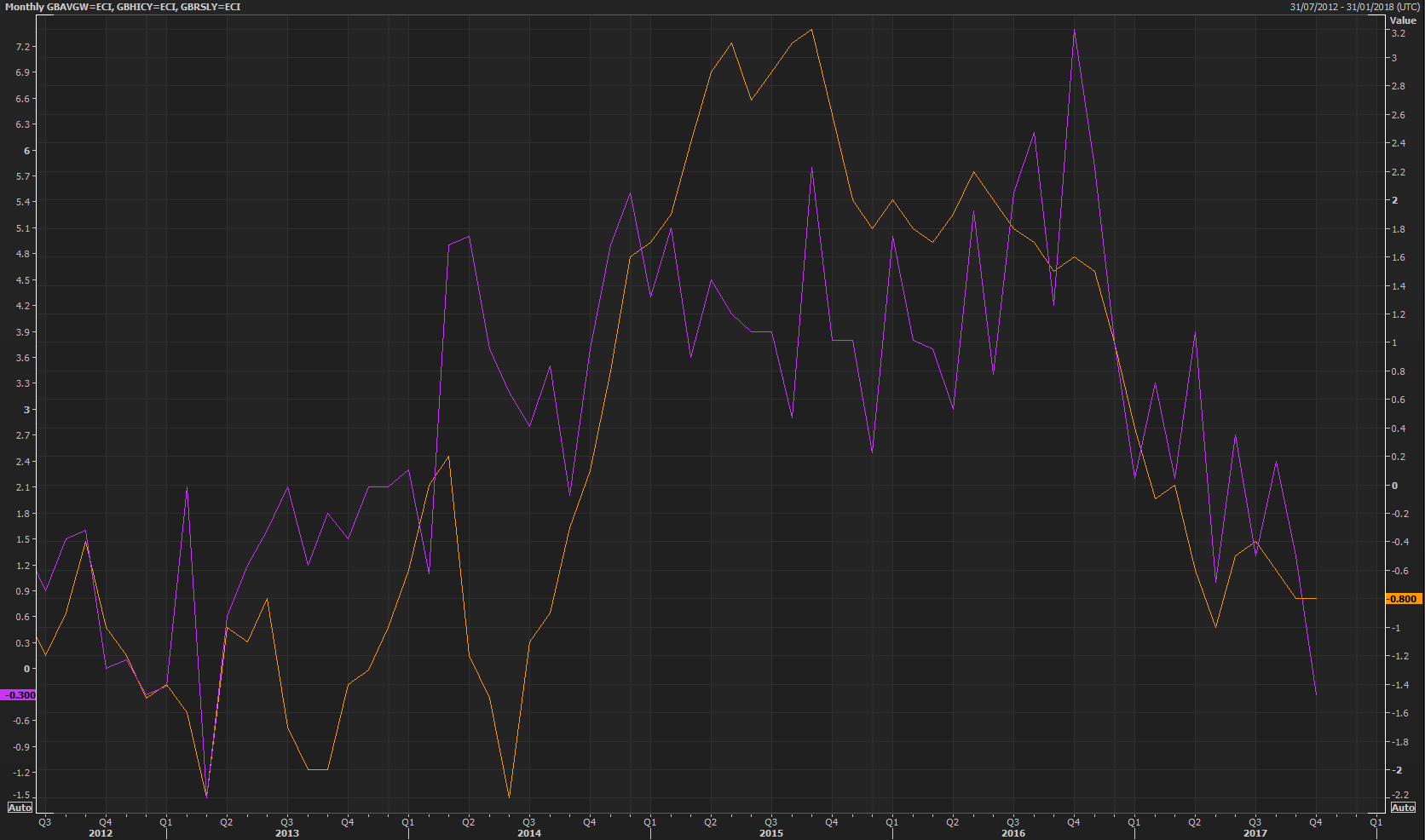

UK retail sales data gave the pound a small boost this morning, despite the numbers themselves being far from desirable. Consumer spending fell by 0.3% in October compared to a year ago – both overall and on a core basis – which was slightly better than expected but also marked the first decline in four and a half years, when the UK was fighting to stay out of recession.

Real Wage Growth (Orange) vs Retail Sales (Purple)

Source – Thomson Reuters Eikon

While the slowdown in consumer spending comes as no surprise given the negative wage growth that has held the economy back since the start of the year, a worrying trend has formed that will likely weigh on economic output in the coming quarters. The pound may well have been given a small lift by today’s numbers but the reality is that the near-term impacts of the Brexit vote are being felt and there’s little to suggest the worst has passed. The FTSE is underperforming its peers this morning, weighed down by sterling’s ascent, as well as general weakness that we’re seeing across the commodity space.

OANDA fxTrade Advanced Charting Platform

US Data and Central Bank Speakers Eyed

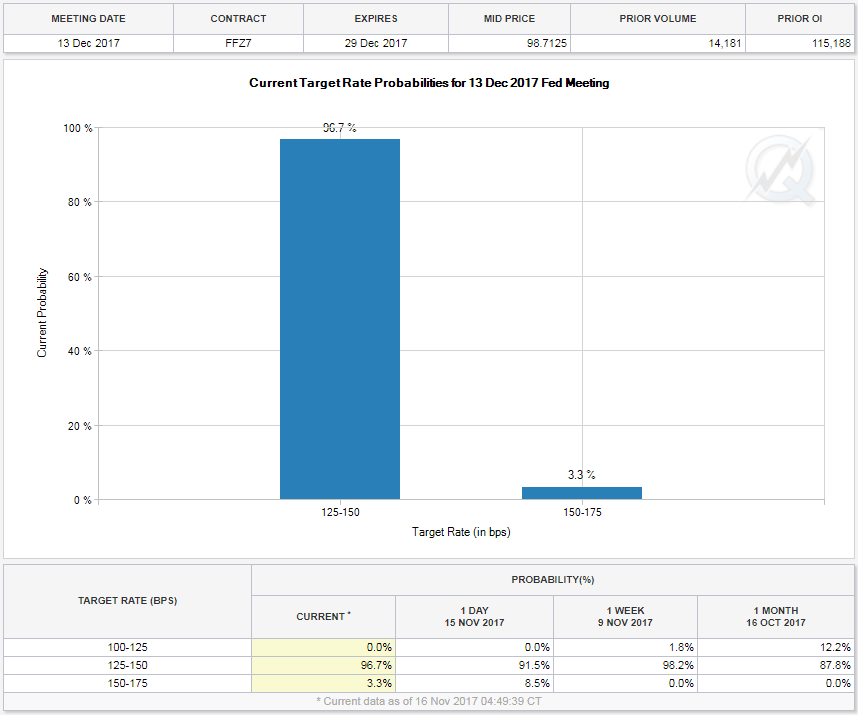

There’s no shortage of economic data and central bank speakers on the agenda today, with jobless claims, the Philly Fed manufacturing survey, industrial production and capacity utilisation data all being released ahead of the open. The data comes as the Fed prepares to raise interest rates again in December – which is almost entirely priced in – although when it comes to next year, markets are very much under-pricing what the Fed has proposed.

Source – CME Group FedWatch Tool

While this has been a common theme over the last few years, it would suggest that markets may have some catching up to do, particularly if Donald Trump can get tax reform through, with it currently running into some stumbling blocks in Congress.

The CPI and retail sales data we got from the US on Wednesday was certainly supportive when it comes to further rate hikes, with the trend in both having improved following a rough start to the year. There are still understandable doubts about whether the Fed should still pursue tightening at the current pace due to the inconsistency in the data but as long as the data remains on a positive trajectory, I don’t see it deviating from the current path, not yet anyway.

Eurozone Inflation Unrevised For October

We’ll get plenty of views on this today, with four Fed officials scheduled to appear including Lael Brainard – a permanent voter on the FOMC – Robert Kaplan – a voter this year – and John Williams and Loretta Mester, both of whom will be voters next year. With a number of positions still to be filled as Trump continues to shape the central bank as he wishes, the consensus view on the committee could change so it’s well worth paying attention to those that will have the vote next year. These will be joined by policy makers from the ECB and Bank of England who are also scheduled to appear throughout the day.

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024