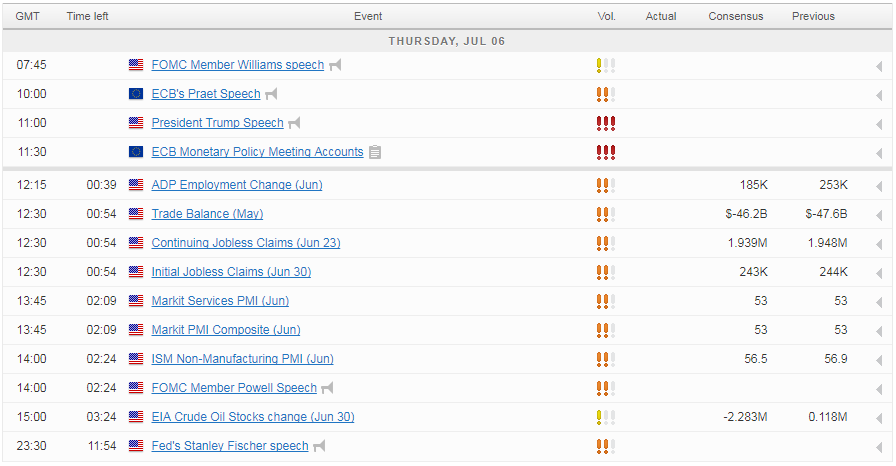

As we enter the business end of the week, the US will be in focus with a large number of data scheduled to be released including some important labour market numbers and surveys on the services sector.

ADP, PMIs and Fed Speakers Scheduled for Thursday

The Independence Day bank holiday earlier in the week caused a delay in a number of figures being released. It means that ahead of tomorrow’s jobs report, we’ll get the ADP release for June which is expected to show 185,000 jobs being created, roughly in line with the NFP 12-month average. This would suggest the labour market is continuing to tighten, giving further ammunition to the hawks on the Fed that argue that inflation will ramp up.

DAX Loses Ground as German Manufacturing Report Misses Expectations

We’ll also get the final services PMI number for June, alongside the composite PMI and the ISM non-manufacturing PMI. The services sector is hugely important to the US economy and both of these numbers continue to point to decent, albeit uninspiring, levels of growth. Jobless claims and trade balance numbers will also be released alongside these figures. We’ll also hear from three Federal Reserve policy makers, with vice Chair Stanley Fischer, Jerome Powell and John Williams all scheduled to appear.

USD Edges Lower After FOMC Minutes

The dollar is trading a little lower on the day as the US open approaches. The minutes from the last FOMC meeting did little to support the greenback, with the lack of inflationary pressures appearing to be taking its toll on the appetite for more rate hikes, among some policy makers. That suggests to me that, while one more rate hike may come this year – perhaps in December – the pace beyond then may slow, with the focus then turning to the balance sheet. Of course, should inflation move towards 2%, as remains the assumption of the committee, the pace of tightening may increase with it.

ECB Minutes Key for Next EUR Move

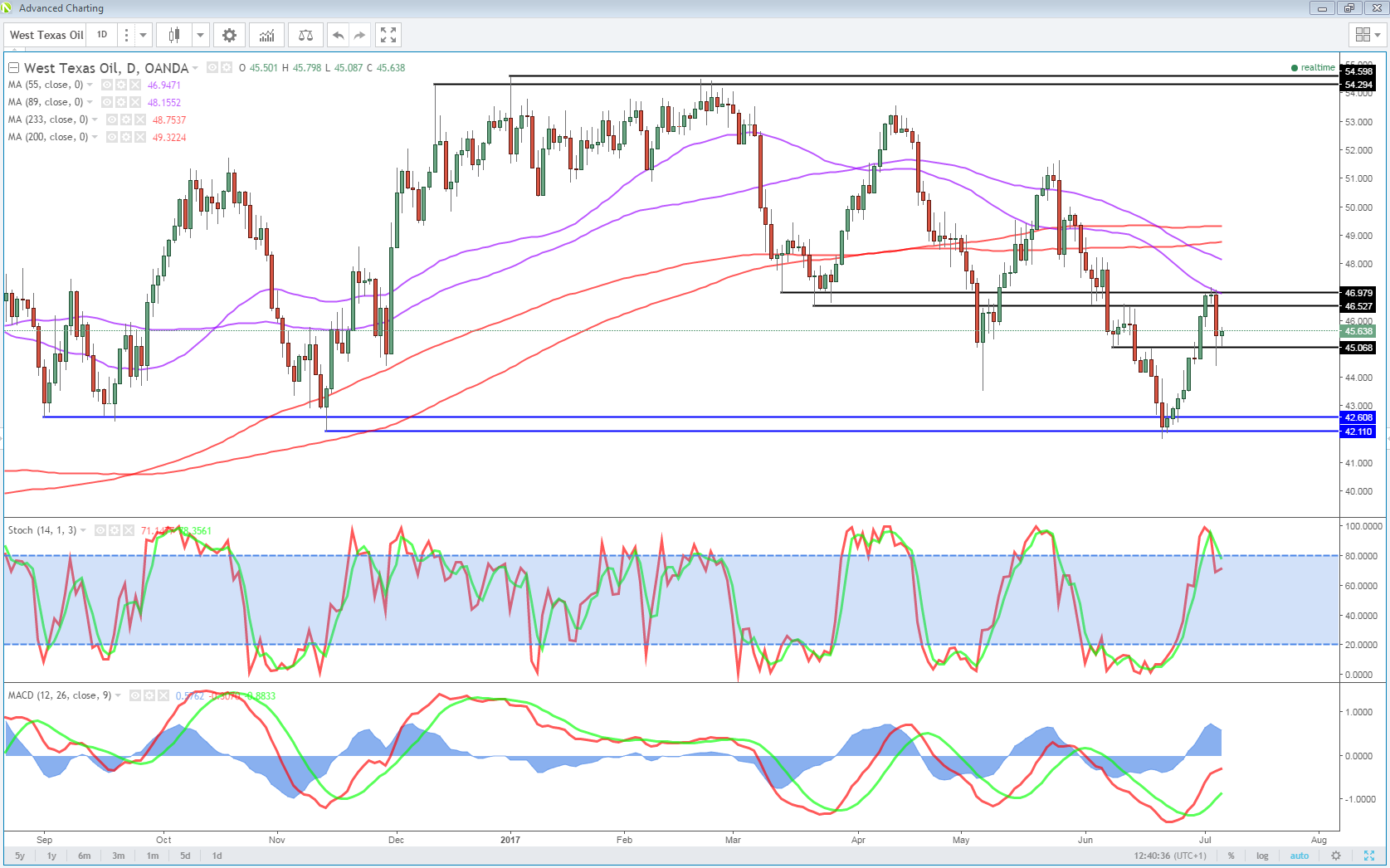

Oil Higher as API Reports Large Drawdown

Oil is up more than 1% on the day so far, paring Wednesday’s losses which came on reports that Russia is not willing to deepen the production cuts that could be necessary to bring the market back into balance and support prices. The rebound off the lows was aided by the inventory data from API which reported a substantial drawdown last week of 5.76 million barrels. Prices may be further supported today if this number is confirmed by EIA, with only around half that currently expected.

OANDA fxTrade Advanced Charting Platform

Economic Calendar

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024