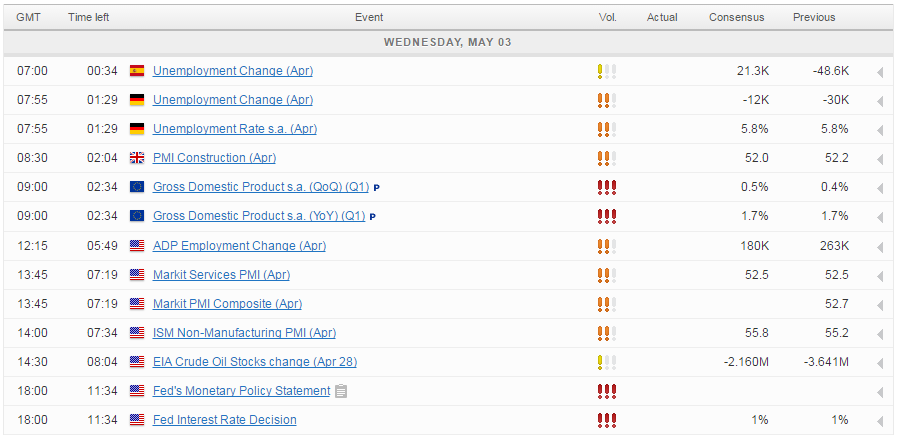

European equity markets are expected to open relatively flat on Wednesday as we await the release of GDP data from the eurozone, unemployment data for Germany and Spain and the construction PMI for the UK.

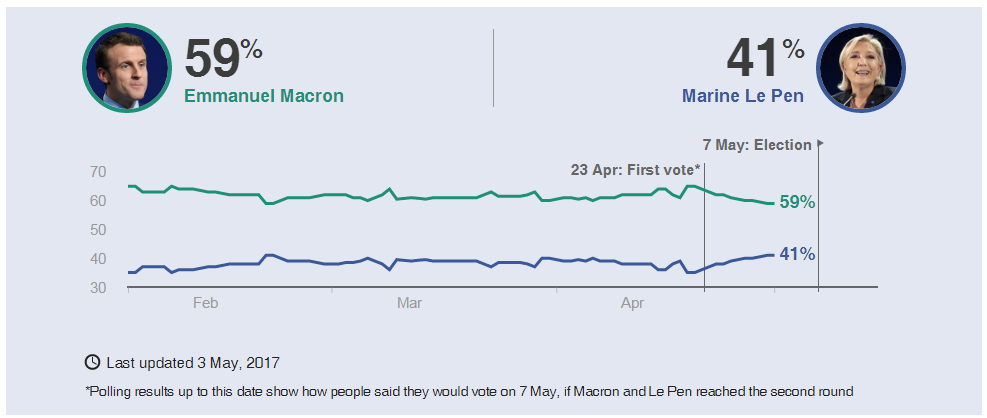

Needless to say, it should be quite a lively morning in Europe, despite the uninspiring open. The eurozone is expected to have grown 0.5% in the first quarter, a decent number given the ongoing challenges facing the region. One challenge that it appears to be overcoming is the rise of populist parties, with the French looking to follow in the footsteps of the Dutch this year in selecting a pro-EU candidate for President. Emmanuel Macron still holds a commanding lead over Marine Le Pen in the polls ahead of voting this Sunday.

The polling average line looks at the five most recent national polls and takes the median value, ie, the value between the two figures that are higher and two figures that are lower.

Source – BBC

French Election Timeline

May 3 – TV debate between the two remaining candidates

May 5 – [from midnight] Poll blackout

May 7 – Second round of French presidential elections. Last polls close at 19:00 BST / 14:00 EDT, with an exit poll result announced immediately.

May 11 – Official proclamation of the new President.

May 14 – [from midnight] End of Francois Hollande’s mandate

June 11 – First round of legislative elections

June 18 – Second round of legislative elections.

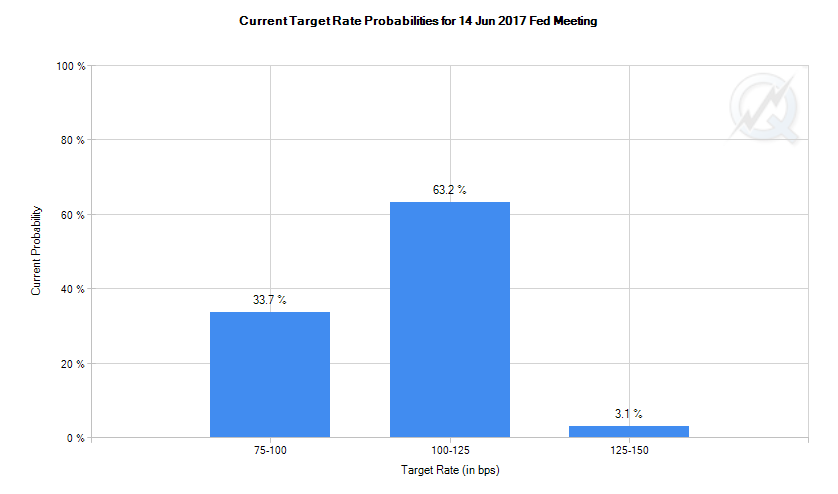

While the Fed decision itself may not surprise anyone – with markets pricing in only a 5% chance of a rate hike this evening – the statement could offer important clues on the central banks intentions at upcoming meetings. In the absence of a press conference with Chair Janet Yellen, the statement is all we have to go off and if the Fed is aiming to raise rates again in June, it may signal its intention to do so.

Oil’s Dead Cat Bounce Ahead of Crude Inventories

Fortunately, with markets already pricing in a June rate hike at 66%, the Fed doesn’t have to work as hard to manage expectations as it did earlier this year and so any signal may be fairly subtle.

Source – CME Group FedWatch Tool

While I expect the central bank to see through the first quarter weakness in the economy, it may refrain from sending a stronger signal in order to give itself room to manoeuvre, should the data not improve between now and the June meeting.

Given the trend that we’ve seen in recent years of the first quarter disappointing, I would expect to see a similar rebound in the data over the coming months. The jobs data on Friday is expected to report a rebound in hiring following March’s surprising increase of only 98,000. Today’s ADP release may offer some insight into what we could see here on Friday, although it should be noted that last month it indicated that 263,000 jobs were added in March, not quite in line with the official data. The final services and non-manufacturing PMIs will also be released this afternoon to wrap up a busy session for the US.

This afternoon we’ll also get the latest inventory data from EIA, a day after API reported a 4.15 million barrel drawdown helping oil prices bounce off their lowest levels since November. With Brent crude testing the psychologically significant $50 level, the inventory data could be a big test of sentiment in crude, with a break of this being rather bearish.

OANDA fxTrade Advanced Charting Platform

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024