European equity markets are expected to open marginally higher on Tuesday as traders await a number of economic reports, while keeping one eye on some key central bank events later in the week.

With the worst of the quiet summer period now behind us and US traders returning from the bank holiday weekend, we can expect to see trading volumes pick up significantly this week, just in time for a number of key central bank events. Between BoE Governor Mark Carney’s appearance before the Treasury Select Committee on Wednesday, the Bank of Canada decision shortly after and the ECB on Thursday, we’re certainly not short of market moving events this week.

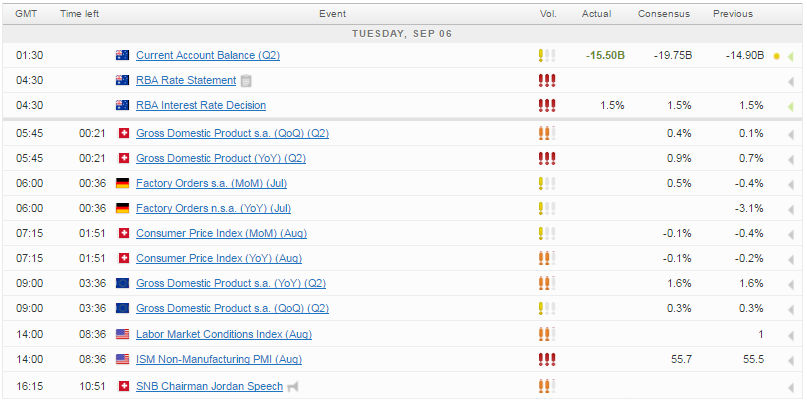

It’s going to be one of the quieter days for economic data, with the bulk of the important releases coming this afternoon when the US returns from the long weekend. Eurozone revised GDP for the second quarter and German factory orders for July stand out this morning but both are likely to be low to medium impact events given the relatively outdated nature of the releases and the fact that no revision is expected for the GDP number. German factory orders are expected to rebound slightly having been on a downward trajectory since March, culminating in a 3.1% annual decline in June.

This sets us up nicely for the return of the US, with the ISM non-manufacturing data being released. The services sector is hugely important to the US economy and so this data offers important insight into how the main engine of growth is likely to perform in the months ahead. While the number is forecast to remain solid for another month – at 55 – the trend of slowing growth that we’ve seen over the last year is expected to continue.

This doesn’t bode too well for the US given the disappointing levels of growth experienced in the first half of the year. The official services PMI, released over the weekend, also confirmed a trend of slowing growth in the sector, attributing it to global uncertainties and the upcoming Presidential election. It will be interesting to see if the same feedback is seen in the ISM data. If so, it doesn’t suggest we’ll see the bounce back in the third quarter that many are hoping for.

Gold – Moving Average Bands Offer Direction Clues

The Australian dollar is trading around half a percentage point higher after the Reserve Bank of Australia refrained from cutting interest rates for a second consecutive meeting. The statement that came alongside the decision didn’t directly hint at the need for further stimulus in the near term but still left the door wide open, highlighting the low levels of inflation, mixed labour market indicators and the complications stemming from an appreciating exchange rate. While I’m not convinced we’ll see another rate cut this year, one remains very much a possibility.

The full RBA statement can be found here.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024