European equity markets are expected to open a little lower on Tuesday following yet another mixed session in Asia overnight, as the Reserve Bank of Australia became the latest central bank to ease monetary policy at its meeting this month.

The 25 basis point rate cut from the RBA, taking the cash rate to an all-time low of 1.5%, was all-but priced in it would appear and came as little surprise to investors. It seems the persistent low levels of inflation tipped the RBA over the edge, with slow global and moderate domestic growth, and the stronger Australian dollar also contributing to the decision to loosen monetary policy further.

The statement from Glenn Stevens, RBA Governor, can be found here.

The response in the markets to the decision has been minor as the move itself was already broadly priced in. The Australian dollar is only trading marginally lower on the day while the ASX has failed to receive any boost at all from the announcement, down around 0.5% on the session. It seems the RBA may have to do more at the upcoming meetings if it really does want to keep its currency low and boost inflation.

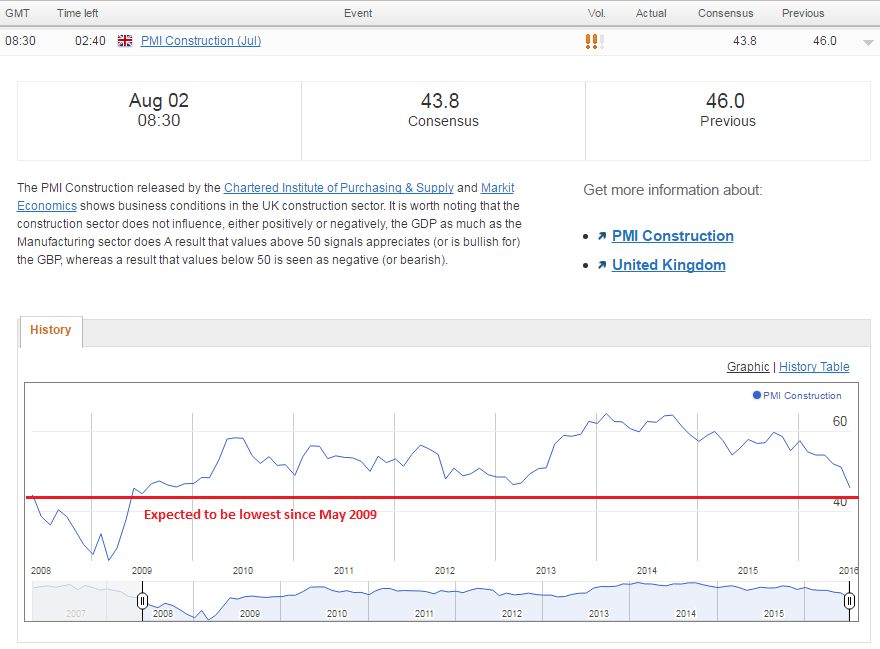

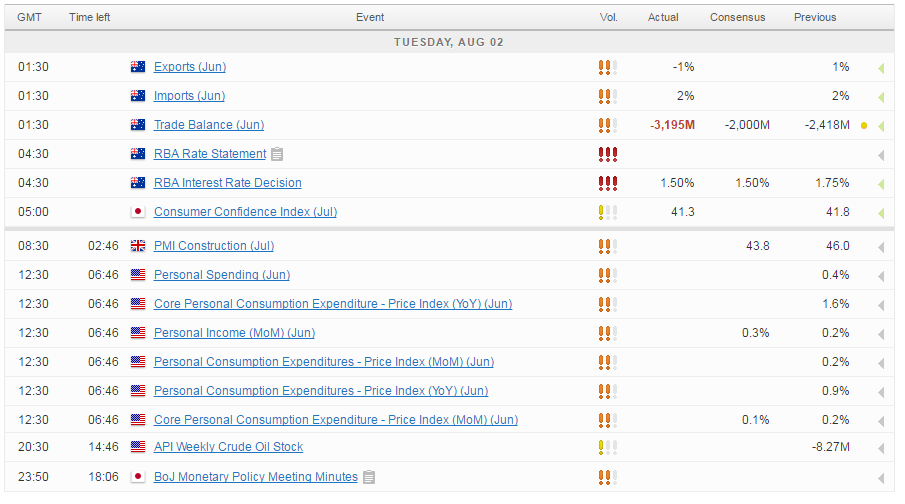

The RBA isn’t expected to be the only active central bank this week. The Bank of England meets Thursday and it is widely expected to ease monetary policy in an attempt to combat the Brexit impact early. The construction PMI data for July is likely to offer further evidence of the BoEs need to act soon, with the number seen falling even deeper into contraction territory – expected at 43.8 – as the first casualty of the Brexit vote shows signs of falling even further into decline.

Source – MarketPulse Economic Calendar

While many investors may already be eyeing up Friday’s U.S. jobs data, today’s income, spending and inflation figures should not be overlooked and will also be very influential when the Federal Reserve is deciding whether or not to raise interest rates at the coming meetings. The core personal consumption expenditure price index is the Fed’s preferred measure of inflation and so this is what they will be looking to for evidence that price pressures are finally starting to appear. As it turns out, we’re not expecting to see much evidence of that today, with the index seen rising only 0.1% from last month.

Spending and income figures also offer essential insight into possible future inflationary trends. One important reason behind the lack of inflation in recent years has been weak income growth, which has likely weighed on spending and therefore inflation. We’re not seeing much evidence of this improving at this stage despite labour market conditions becoming much tighter in recent years.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024