We’re continuing to see a little risk aversion in the markets on Tuesday, with investors adopting come caution ahead of this week’s key risk events, the Federal Reserve and Bank of Japan meetings.

European equity markets are currently on course to open a little higher but these gains are marginal and at this stage only represent a slight paring of Monday’s losses. Weakness in commodity markets – usually associated with the risk-off trade – weighed on indices on Monday and again during the overnight session in Asia, and could continue to do so throughout trade today.

Oil is currently trading around half a percentage point higher on the day but remains down on the week after Genscape reported on Monday that inventories in Cushing rose again last week. This could be confirmed by API when it releases its figures this evening and EIA on Wednesday, which could weigh further on oil prices. Oil has been surprisingly resilient given the news flow over the last week, it will be interesting to see if it continues to do so if this rise in inventories is confirmed this evening. If so, it could send a very bullish message to the markets.

The yen is trading higher again in the run up to Thursday’s policy decision from the BoJ. Of course, the gains since the start of the week pale in comparison to Friday’s moves and in reality possibly just represent a little bit of profit taking ahead of the announcement. Given the risk-off environment that we’re seeing at the start of the week, it could also be benefiting from its safe haven status. Whatever the reason, the gains are small and come Thursday, I expect to see much larger moves. Although after the last time the BoJ eased, it’s difficult to be too confident on the direction that will take.

The pound is also building on gains again on Tuesday following what has been a very successful week or so for the “remain” campaign. Between Chancellor George Osborne’s 200-page dossier on the risks of leaving the EU, US President Barack Obama’s warning that a trade deal wouldn’t come easy or fast and the sheer lack of anything from the “leave” campaign, the odds of a “Brexit” have fallen considerably which the pound is benefiting greatly from. It’s still early doors and I’m sure an assault from the “leave” camp is imminent but so far their response has been lacklustre and unless they act soon, they may find themselves with considerable ground to make up.

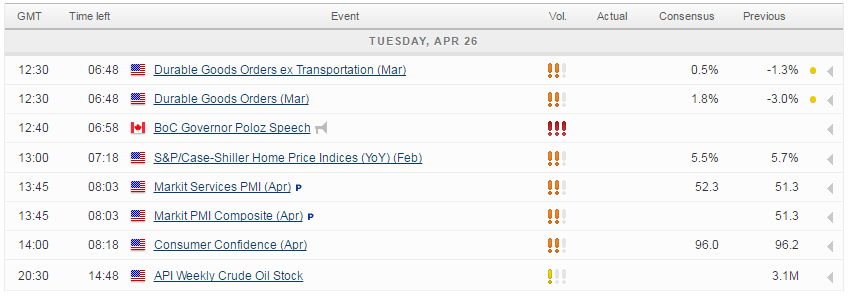

Once again today, there is some economic data due out but investors may have one eye on tomorrow’s Fed announcement and Thursday’s BoJ decision. That said, durable goods orders is a key economic indicator, as is the flash services PMI and CB consumer confidence number so we could get some volatility around these events. It’s also worth remembering that earnings season could continue to play a key role in overall market sentiment and there are a number of companies due to report today including Apple, Procter and Gamble, eBay and BP.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024