European markets are lower across the board on Thursday despite more dovish comments from ECB President Mario Draghi that suggest further monetary easing remains on the table in December. With the Fed looking increasingly likely to raise interest rates which has played a big role in the euro falling from 1.15 against the dollar to around 1.07 today, it was possible that the ECB may have delayed its intentions to ease due to the far more favourable exchange rate. Of course, the central bank is prohibited from basing its monetary policy decisions on exchange rates but it’s clear that the stronger euro was having a deflationary impact on the euro area.

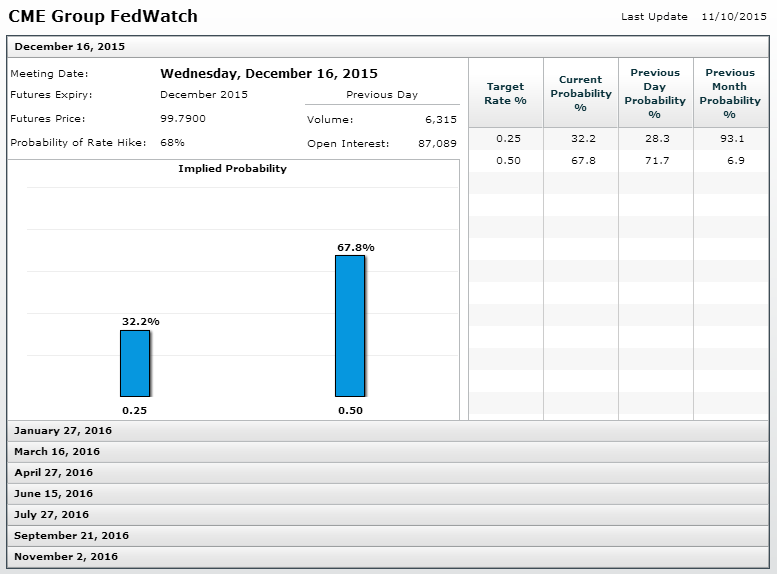

With Draghi appearing to have shown the ECBs hand, it will be interesting to hear the views of the Federal Reserve following last week’s impressive jobs report. The report appeared to tick every box as far as the Fed is concerned which gives them the perfect opportunity to raise interest rates in December. There are a number of Fed officials due to speak today including Chair Janet Yellen and vice Chair Stanley Fischer and it will be interesting to see how influential that jobs report was. Clearly the markets saw it as being extremely influential which is why they are currently pricing in a 68% chance of a rate hike in December and a 32% chance of a second by March.

Source – CME Group FedWatch Tool

It is now up to the Fed to manage expectations in the coming months and to constantly reassure markets that rate hikes will be gradual, as it has repeatedly stressed until now but clearly the markets are beginning to doubt. I expect the message today to be broadly similar to the statement from the October meeting, that December remains a possibility and that the path of rate hikes will be gradual. They may even stress that the jobs report is one small selection of data and that there’s plenty more to come before the next meeting. Under Yellen, the Fed does like to leave the long list of excuses on the table right next to the rate hike, just in case.

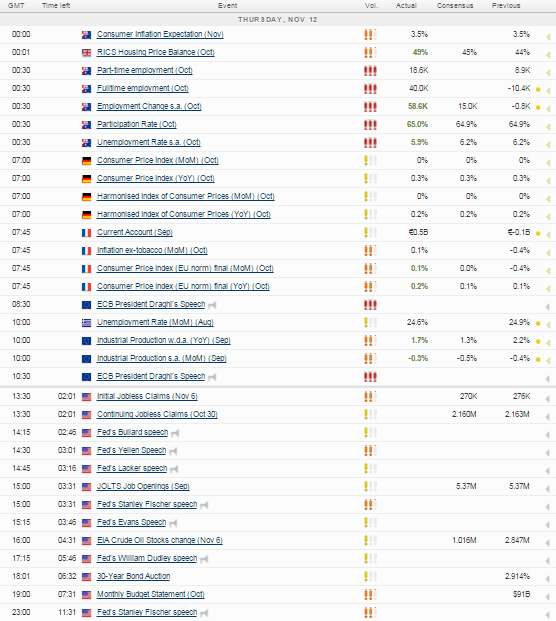

There will also be a focus on the data today with JOLTS job openings for September being released. Of course, given that we’ve already had the employment report for that and the following month, the data is already a bit outdated, but it does offer good insight into the sustainability of job creation in the coming months if the trend of job openings is continuing to rise. We’ll also get the latest jobless claims number today as well as crude inventories data which comes as WTI trades near two month lows. Another strong build in inventories could be what it takes to break back towards $41.30, last seen at the end of August.

The S&P is expected to open 5 points lower, the Dow 42 points lower and the Nasdaq 7 points lower.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024