European bourses are expected to open moderately higher on Monday following a mixed end to trading on Friday and concerning trade figures from China over the weekend. The trade balance figures were the first of a number of Asian data releases this week that markets are likely to take a particular interest in.

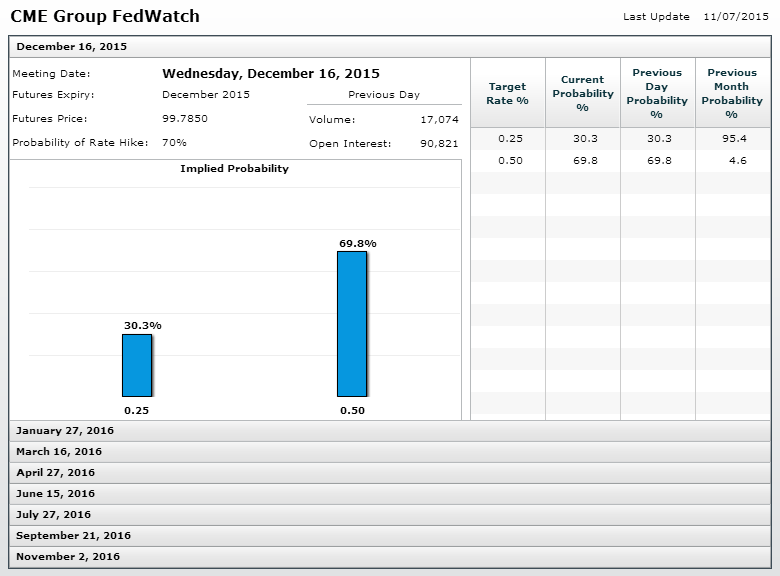

Friday’s U.S. jobs report was much stronger than the markets were anticipating which dramatically increased the chance of Federal Reserve tightening at the December meeting, according to Fed Funds futures. The probability of a rate hike now stands at around 70%, up from around 58% ahead of the report and 35% prior to the meeting a couple of weeks ago. With only a couple of notable pieces of data coming from the U.S. this week, we could see focus shift to emerging markets and how they are coping with the increased probability of a rate hike, especially when we’re simultaneously getting reports on the regions cooling economies.

Source – CME Group FedWatch Tool

Back in August, fears over a rate hike sent emerging markets into a frenzy and while the result of this was hopefully that a rate hike is now already priced in, we can’t write off the possibility that more panic will ensue. Moreover, Friday’s jobs report did not just prompt an increased pricing in of a December rate hike, we also saw the odds for a second hike in April rise quite significantly as well. The prospect of recurring hikes could be what makes emerging market investors nervous once again.

Many markets in Asia are in the red at the start of the week but there’s no sign yet of panic. More importantly, Chinese indices are currently performing very well which at least for now may help ensure some stability. Although as we’ve seen on many occasions in the past, that can change in a heartbeat so we shouldn’t get complacent.

Another poor batch of trade data overnight appears to have done nothing to shake investor confidence in China, despite a significant drop in both imports and exports being behind the record trade surplus. Other countries in the region haven’t shaken this off so well given that they depend heavily on China for trade but maybe the possibility of more stimulus from the People’s Bank of China on the back of this is enough to keep investors happy. I’m sure this will be tested more than enough this week with inflation, industrial production, fixed asset investment and retail sales data all to come.

In Europe we’ll get the latest trade data from Germany which should shed further light on how the slowdown in emerging markets and weaker demand in China is impacting the country’s exporters. We’ll also get the latest Sentix investor confidence reading which is expected to rise slightly to 13.2.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024