Impressive Growth in Q2 Was Not Enough for Fed to Hike Rates

The U.S. dollar has regained some the ground lost after the Fed’s decision to keep rates on hold in the September Federal Open Market Committee (FOMC) meeting. The trend does not have the same momentum as before the rate setting meeting and improving economic indicators will be used to second guess the decision from the American central bank to not hike interest rates. The USD continues to be weaker when compared to major pairs, specially those nations where central banks have been pressured to act after the Fed inaction such as the Bank of Japan and the European Central Bank.

The Final gross domestic product (GDP) will be released on Friday, September 25 at 8:30am EDT. This is the third and final GDP release published 85 days after the end of the quarter. The U.S. economy had a terrible first quarter so all eyes in the market were keen on spotting signs of a recovery as the advanced and preliminary GDPs were announced. The first quarter data was revised from a contraction into a slight expansion of 0.6 percent.

The GDP in the second quarter has exceeded expectations and is on track to record 3.7 percent growth in line with the second estimate. The Commerce Department revised the advanced GDP number from 3.2 percent but the final number should be closer to the advanced report. Improving GDP was one of the factors the market was counting on to persuade the Federal Reserve to deliver its much-awaited interest rate hike. The final GDP figures, will probably have a subdued impact on the USD as even exceeding expectations would do little to boost the currency.

Global stocks traded lower as Chair Janet Yellen is due to take the stage to talk about “Inflation Dynamics and Monetary Policy”; at the University of Massachusetts. The market will be waiting for more insight on the timing of the rate hike. Anything less, specially a repeat of the press conference following the FOMC will be seen as a negative to the USD as investors are looking for clarity, not more rhetoric.

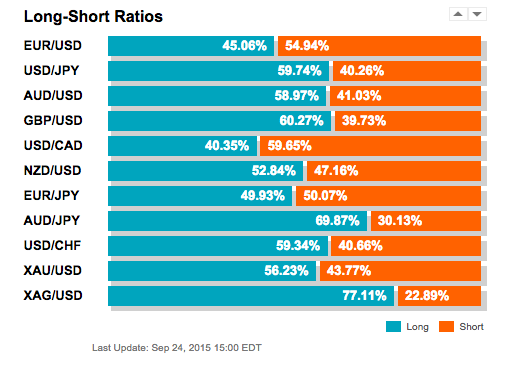

The OANDA Open Orders Ratio illustrates the confusion that has been sowed by the Federal Reserve following their September meeting. The 45 percent long to 55 percent short is too close as investors pick a side of the currency pair. If Janet Yellen does not add clarity to the timing of the rate hike, which is what the market anticipates given the silent treatment from the chair of the Fed this year, then the market will look back to the data for direction but not without punishing the USD. Next week the non farm payrolls report will be published which could make a bolder point that Fed member verbal intervention could.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Alfonso Esparza

Latest posts by Alfonso Esparza (see all)

- Market Rally Still Going Low Holiday Volumes Awaiting Start of 2020 - 27 December 2019

- Market Awaits China Retaliation on Trade - 29 November 2019

- Alibaba to Close Order Book Ahead of Huge IPO - 18 November 2019