This week looks set to end on a slightly positive note with European futures pointing to a moderately higher open following similar gains in the U.S. and Asia overnight.

Risk appetite has certainly improved this week although we’re still seeing investors hold back a little. Clearly there is still some fear that the markets could just implode again and all of the factors that were supposedly behind the first round are still very much still there. That said, investors may see more opportunities now than they did before which could support markets at these levels.

One of the key risks all along has been the Federal Reserve and whether it will raise interest rates at the meeting next week. The debate has been going on for months and there are plenty of arguments for and against it. Moreover, many Fed policy makers appear on the fence so it’s hardly surprising that there is so much uncertainty surrounding it.

In fact, the uncertainty is causing more problems in the markets than the prospect of a rate hike itself. This view is increasingly shared by many emerging market central bankers who think the Fed should just raise rates already and remove the uncertainty from the markets.

With the meeting fast approaching, we could see a little more caution in the markets between now and next Thursday’s decision. Whatever the announcement, the market reaction is likely to be substantial and that can make some investors uncomfortable.

That could extend to today with a number of pieces of Chinese economic data being released over the weekend. So much of the recent market turmoil has come from China and this data could be the latest trigger. The fact that it is released when the markets are closed may prompt some risk aversion into the close today. These are some key data releases and could dictate sentiment at the start of the week.

While we may see some added caution over the next week and possibly some risk aversion into the close today, that doesn’t mean the session will be dull. There are a number of important pieces of data being released that could provide some market volatility.

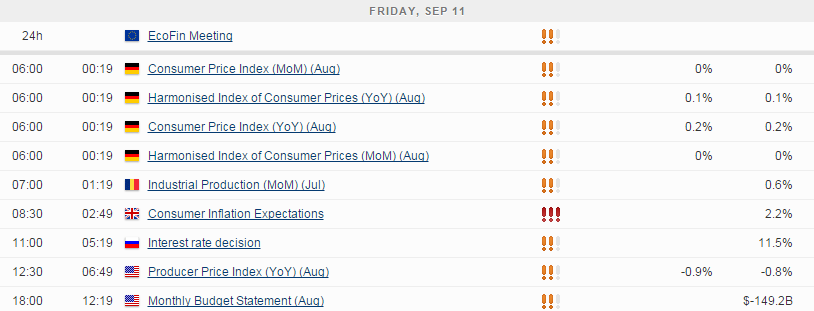

We’ll get final inflation figures from Germany and Spain early in the session, followed by U.K. consumer inflation expectations, a very important indicator of future inflation. In a period of low inflation, it is important for inflation expectations to remain high or the consumer may start putting off large purchases and wait for cheaper prices, or just not be worried about them rising much. In a country like the U.K., that could lead to some serious problems and consumer spending is so important to the economy. While inflation expectations have been falling over the last few years, they are still above 2% and therefore are not currently a concern.

Later on in the U.S. we’ll get PPI inflation data followed by the preliminary UoM consumer sentiment reading for September.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024