European indices are expected to open lower on Thursday following a less than impressive lead from the U.S. and Asia overnight.

Disappointing data in Asia appears to be weighing on sentiment today. Of course, sentiment is very fragile right now so it doesn’t take much to knock it. That said, a second straight month of decline in core machinery orders in Japan is a concern as it shows that capital investment among companies is seriously lacking. We were expecting a decent rebound following last month’s sharp 7.9% decline but instead we got another substantial drop.

This raises all sorts of concerns about the desire of businesses to invest and whether this reflects a more pessimistic outlook, driven by weak demand both domestically and from abroad given China’s apparent slowdown. It doesn’t bode well for Prime Minister Shinzo Abe’s plan to bring inflation back to 2% either, if businesses are pessimistic and aren’t investing then wages are unlikely to rise much.

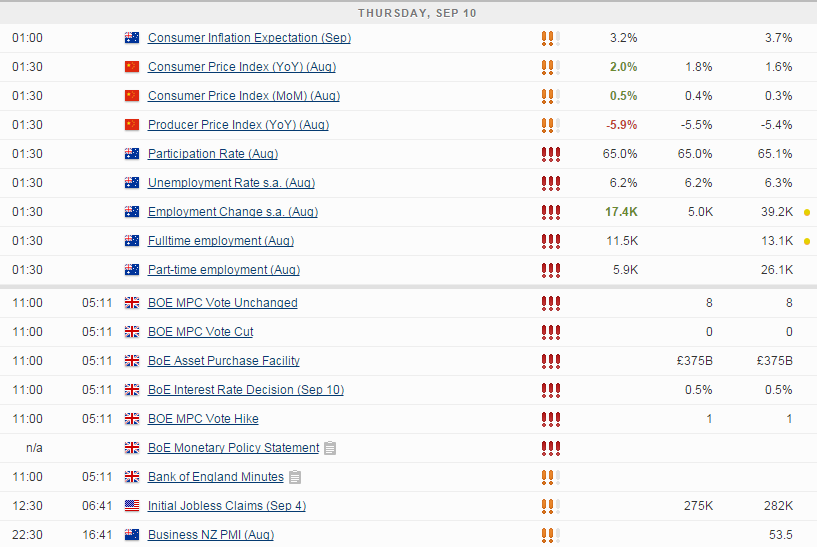

Chinese inflation rose to 2% in August, above expectations of a rise to 1.8%, driven largely by higher food prices, in particular pork. The rise was not enough to ease the concerns of investors though as producer prices fell much more than expected – 5.9% – increasing the risk of the economy experiencing deflation further down the road.

The Bank of England is expected to keep interest rates and asset purchases unchanged when it announces its latest monetary policy decision this afternoon. There has been a more hawkish tone coming from the Fed in the last few months despite the persistent low levels of inflation, which suggests that there is a strong desire among policy makers to begin the move back to normalisation as soon as possible.

This is very similar to what we’re hearing from the Federal Reserve and in fact, today’s outcome could offer some clue as to how its meeting will go next week. Policy makers from both central banks have claimed recently that the Chinese slowdown and the related events of the last few weeks should not have a significant impact on their economy. We should find out today whether this is a view shared by all and if it has created enough of a stir to delay any rate hikes from taking place.

The key giveaway could be whether Ian McCafferty votes for a rate hike again or not. If he doesn’t and the vote is unanimous then surely it would suggest that policy makers are keen to see this play out before making a judgement call, a view likely to be shared by their counterparts across the pond. Of course the minutes should shed further light on this.

The U.K. economy itself appears to have cooled since the last meeting which may also influence policy makers, although one month in isolation is unlikely to affect their judgement too much. Still, weak retail sales, declines in manufacturing and services PMI readings and disappointing industrial production figures are going to be of concern. On the bright side, the core CPI picked up a little and wage growth remains decent at 2.4%, easily outstripping inflation.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024