U.S. indices are expected to open significantly higher following the long bank holiday weekend. The move follows strong gains at the start of the week in Europe while Asia also saw some impressive gains overnight, most notably in China in the final couple of hours of trade.

This strong end to the session came despite China releasing worrying trade figures overnight which suggests either traders are banking on further stimulus measures from the People’s Bank of China or we’re seeing more government buying to support and stabilize the markets. The trade figures once again highlighted a worrying trend in China, which is attempting to transition from an investment dependent economy to one driven by the consumer.

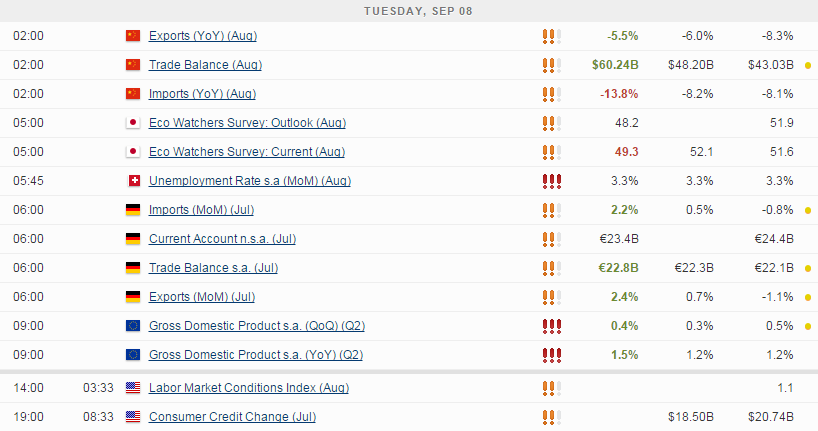

While we are seeing the expected slowdown in exports, albeit at a faster pace than many may have expected – down 5.5% in August from same month last year – imports are falling at an even faster rate which is very worrying. Of course, this can be partly attributed to falling commodity prices with import and export figures being denominated in dollars, but lower domestic demand is also contributing to it. If the consumer cannot fill the void left my falling export demand, then the government has a big job on its hands to stop the economy slowing at a much faster pace.

Eurozone growth in the first and second quarter was better than initially thought, with Q1 GDP being revised up to 0.5% and Q2 up to 0.4%. Expectations were for the numbers to remain unchanged so this is likely to be helping to lift sentiment in Europe this morning. Of course, annual growth of 1.5%, up from initial estimates of 1.2%, is still nothing to get carried away with. The economy remains very fragile and vulnerable to internal and external shocks, as we saw in the first half of the year when uncertainty surrounding the future of Greece knocked sentiment in the region. China could continue to weigh on the eurozone recovery in the coming quarters.

U.S. investors return on Tuesday following the Labor Day bank holiday. The first day back could be a little quiet on the economic data side but there is plenty for investors to respond to given the late rally in China overnight. We could also see some delayed reaction to Friday’s jobs report which gave both hawks and doves something to cling on to.

Next week’s Federal Reserve meeting will remain at the forefront of trader’s minds in the trading sessions ahead and any data releases are likely to get a lot of attention. A rate hike looks unlikely at this stage given the recent China-driven market volatility and the mixed data seen in recent months, but it is certainly not off the table so any data releases will be monitored closely. Today we’ll get labour market conditions and consumer credit data which will provide further insight into the U.S. economy.

The S&P is expected to open 40 points higher, the Dow 326 points higher and the Nasdaq 90 points higher.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024