US futures are pointing higher as we approach the final trading session of the week, following yesterday’s big sell-off on Wall Street which appeared to be triggered by a combination of weak earnings and rate hike fears.

Wednesday’s minutes really appear to have worried investors. I think people had begun to believe that the Fed would hold off on rate hikes until next year because of the weakness experienced in the first quarter but Wednesday’s statement suggests that is far from the case. When rate hikes are being discussed alongside weak earnings reports, it’s not surprising that investors are getting a little anxious.

While futures may be moving higher today, I think this is just stocks paring losses from the last couple of session. We’ve seen time and time again this year that when indices are trading around record highs, investors begin to feel uncomfortable. That does not suggest there is a confidence in the markets that there is much upside potential left. If the 17 April lows of 2,081 in the S&P and the 17,748 Dow can be broken in the coming sessions, I worry that a much larger correction could follow.

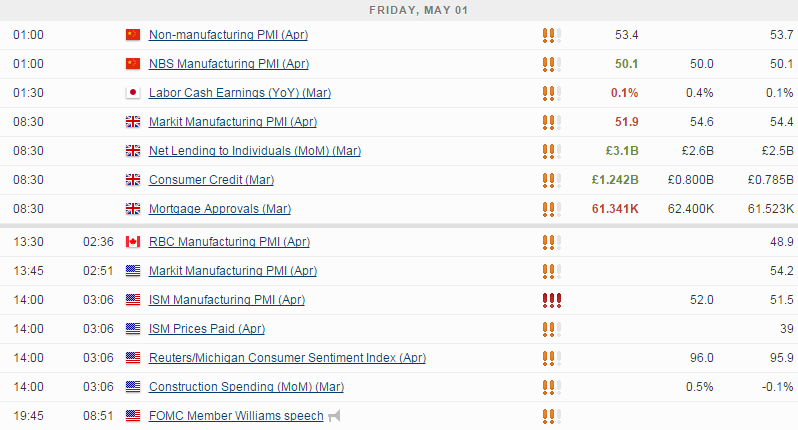

Trading volumes may be lower today as a result of the bank holiday in much of Europe but we’re still seeing some interesting moves in the markets. Sterling is under pressure this morning following a big miss in the April manufacturing PMI that once again highlighted the UK’s dependence on the services sector – which makes up 78.4% of the economy – to drive economic growth. I’m not sure which component of the report was most worrying, output or prices. Manufacturers are being forced to lower prices as a result of falling overseas demand and I don’t expect this to change any time soon.

We’ll get two similar PMI reports from the US, the official PMI reading and the ISM reading. The ISM number tends to carry a little more weight in the markets as the official reading is a revision of last week’s preliminary release. It is seen rising slightly to 52 in April which is still quite low compared to the levels seen last year. I would hope that if we are going to see a rebound in the economy in the second quarter that this number will pick up a lot more but the US will be facing the same overseas demand challenges that the UK is seeing.

Given the importance of the consumer to the US economy, the UoM consumer sentiment reading will be key. Consumer spending in the first quarter was quite disappointing which has been blamed on the poor weather. This makes me more optimistic about the coming months as lower spending in the first quarter should mean people now have a little extra cash, not to mention the boost to disposable income that the oil price decline has produced. Hopefully this consumer sentiment reading will suggest that spending will pick up significantly going forward.

The S&P is expected to open 6 points higher, the Dow 60 points higher and the Nasdaq 7 points higher.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024