European futures are mixed ahead of the open on Thursday despite the negative lead coming from the US and Asia following a mixed message from the FOMC’s latest policy statement.

As always, people are going to drill into the statement and interpret it in whatever way supports their own particular views. This month’s statement makes that very easy because the more dovish among us will focus on the acknowledgement that growth slowed in the winter months and inflation continues to run below the longer term objective. However, the statement also referred to the slowdown in growth as “transitory” and stated that it expects inflation to gradually rise towards 2% over the medium-term.

This is far more important in my view than a reference to a weak quarter that was driven by temporary factors such as weather and lower oil prices. Even the stronger dollar shouldn’t hit the economy as hard going forward as it did in the first quarter. A rebound in the economy in the second quarter should give the Fed comfort to raise rates and I still believe that will come in September. If the slowdown in the first quarter proves not to be transitory or disinflation pressures grow then we may have a problem, but until then I see no reason for the Fed not to raise rates this year.

The full FOMC statement can be viewed here.

We appear to have seen some big strides forward in negotiations between Greece and its creditors in the last couple of days. Greece’s deputy Prime Minister yesterday suggested that a deal could be done in early May and his language suggested it won’t necessarily be a deal the Greek people will be happy with, referring to it as a “minimum agreement” in order to avoid default while stating that in the long term, not just any solution will suffice. This sounds like fighting talk from a group that has been forced to concede on this occasion.

This is far better than the alternative, defaulting on its debt, which according to one eurozone official was days not weeks away. An eventual Greek default and exit is far from off the radar though, the can has potentially just once again be kicked down the road.

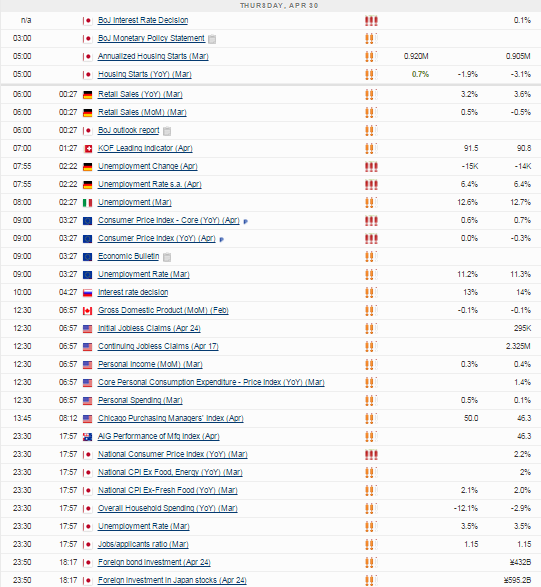

There’s plenty of economic data being released today which should provide a small distraction from the usual Greek chatter. German unemployment data will be released early in the session, with the rate seen remaining at 6.4%, as will inflation and GDP figures for Spain and, most importantly, inflation and unemployment figures for the eurozone. Both are expected to offer good news with deflation believed to have ended in April and unemployment fallen to 11.2%. This would suggest that the ECBs quantitative easing program is having a positive impact, helped largely by the depreciation of the euro.

Later on we’ll get the latest jobless claims, income and spending figures from the US, as well as the core personal consumption expenditure price index number March. This is the Fed’s preferred measure of inflation but comes a couple of weeks after the CPI release and therefore doesn’t get the kind of market reaction you would otherwise expect.

The FTSE is expected to open 9 points higher, the CAC 7 points lower and the DAX 19 points higher.

For a look at all of today’s economic events, check out our economic calendar.

Content is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Business Information & Services, Inc. or any of its affiliates, subsidiaries, officers or directors. If you would like to reproduce or redistribute any of the content found on MarketPulse, an award winning forex, commodities and global indices analysis and news site service produced by OANDA Business Information & Services, Inc., please access the RSS feed or contact us at info@marketpulse.com. Visit https://www.marketpulse.com/ to find out more about the beat of the global markets. © 2023 OANDA Business Information & Services Inc.

Former Craig

Latest posts by Former Craig (see all)

- Market Insights Podcast – US GDP, RBNZ holds, bitcoin soars - 28 February 2024

- Market Insights Podcast – Nvidia earnings, record highs for stocks - 23 February 2024

- EUR/USD – A bullish breakout or just further consolidation? - 22 February 2024