USD/JPY breached 103.0 yesterday following rumors that BOJ will be seeking to increase current stimulus package. Governor Kuroda was seen yesterday saying that the Central Bank will keep its commitment to hit the 2% inflation target in 2 years, fueling speculation that BOJ may even go beyond buying Japanese Government Bonds (JGBs) and purchase riskier products such as stock-market-linked funds in order to achieve its target. How this will benefit Japanese economy is a huge question mark, as buying stock-market-linked products will only drive up asset prices higher – possibly giving BOJ the 2% inflation it badly wants. However, how this will then inspire higher level of production/consumption which is needed to drive the Japanese economy is sketchy.

Share prices rising (incidentally Nikkei 225 is at 6 months high currently) does not mean anything, and Japan should have already learnt this lesson from US, where the term “QE” was birthed. US stock prices are at record highs, but unemployment levels remain high, with the economy still about 1.1 million jobs weaker than pre crisis days. In similar fashion, additional QE (dubbed JQE2) from BOJ will shave little off Japan’s current unemployment issues and consumption level slowdown. Yen has indeed weakened due to the artificial liquidity in the market, but there are actually evidences that consumers are consuming less due to the inflated prices in F&B industries – the direct opposite of what BOJ wants: full recovery of Japanese economy.

Hence, Japanese stocks are in a very precarious scenario, and we could see prices falling like a house of cards if BOJ does not address the underlying problems of the economy directly. Currently prices remain buoyant and in fact broadly bullish due to the fact that BOJ is injecting liquidity with the promise of buying up more stocks indirectly (via stock-market-linked funds). Take that away, and we are back to pre-intervetion levels as Japanese economy and overall Corporate profitability (sans extra earnings from exports due to weaker Yen) have not increased much.

What about Yen then?

This is a more tricky issue in the long run. Current weakness in Yen can be attributed to the additional liquidity of BOJ, but one cannot ignore the fact that the need for safe haven currency in 2013 has been on the wane with global stock market going strong. The “Fear Index” Vix is also close to the lows of pre 2007, lending strength to this assertion. Furthermore, USD has strengthened significantly and is slated to strengthen further with the Fed expected to taper QE purchases in 2014. Hence, USD/JPY’s uptrend will remain without BOJ intervention.

However, it should also be noted that the market has given huge premiums to USD/JPY in anticipation of BOJ weakening Yen. Therefore, if the effect of BOJ stimulus is put into question, there will be at least some quarters of traders that may think that Yen should revert back to its previous strength or at least recover some of it. But if we look at the fundamentals – if BOJ stimulus fail to revive the economy, Japan will be condemned to perhaps another long spell of deflation/recession, and that would have a weakening impact on Yen.

Certainly, the direction of Yen become less obvious and hence traders will certainly do well to gauge what is the market focusing on – the fundamentals of Japanese economy, or the failure of BOJ to weaken Yen further. Long-term wise, it is likely that price direction will mean revert back to fundamentals, but there is no telling how market sentiment may impact prices in the next 2 years of BOJ stimulus era.

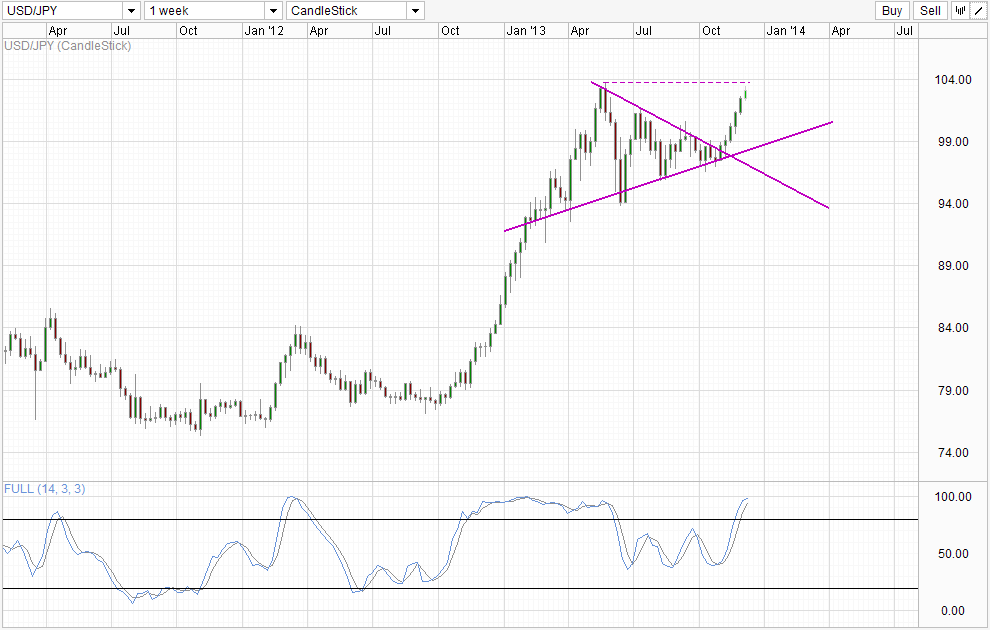

Weekly Chart

From a pure technical perspective though, USD/JPY will be facing resistance in the form of 2013 swing higher around 103.75. Stochasic readings are also heading towards the mathematical limit of 100.0, favoring a bearish pullback in the immediate future. For now it seems that the uptrend is intact, and even if price rebound from 103.75, it is possible that price may find support from 100.5 (which may be the confluence with the rising trendline assuming a mild rate of decline in the next few weeks). This fits nicely with the scenario where BOJ’s additional stimulus fail to excite the market, but instead of despairing market ends up speculating that BOJ will do yet more stimulus in 2014 – a possible scenario which happened back in 2012 before QE3 was announced.

More Links:

GBP/USD – Eases Away from Two Year High towards 1.6350

AUD/USD – Turns Around and Looks Towards 0.90 Again

EUR/USD – Falls back to Key Level at 1.3550

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014