Let’s hope that this is the beginning of a different week where liquidity is deeper and volatility is enough to draw more global market interest. So far, this month has seen very little European interest with the annual holiday season having more of an impact than in recent years. With little in the way of key economic data either side of the Atlantic market moves are likely to be range bound. So far, the overnight tight ranges would suggest ongoing market fatigue. The USD’s performance against its major trading partners remains rather lackluster despite US yields pushing to a new high on Friday. Trading can be described as ‘choppy at best’ as investors wait for the July’s FOMC minutes to be delivered mid-week.

Financial markets have been subjected to intense speculation over when the Fed will begin reining in its $85b a month bond-buying program. The minutes have the potential to generate some volatility in the markets. Many market participants are expecting them to help clarify where Fed officials stood on the subject of tapering as of late July. It is assumed that most policymakers still expected to taper QE3 purchases as soon as September – the growing feeling is that a September move is still on the cards, however, its probably less of a done deal that say a month ago. The “rush-to-buy” the dollar has turned into a “rush-to-wait-to-buy.”

Also this week Stateside is this years Jackson Hole Economic summit where many do not expect the gathering to acquire much market attention due to the lack of a keynote speaker. Capital Markets will be expected to focus mainly on the mid-week FOMC minute’s release, wondering if the US data-to-date should support taper next month. If the minute’s do happen to show a bias to taper at that meeting, it would likely spur a bearish reaction in the Treasury market and cause the USD to outperform, especially against some of the current favored EM shorts (TRY, INR and ZAR).

Better data from G7 members, coupled with the move higher in their bond yields is creating a tough “backdrop for emerging market assets.” India again overnight saw some of the most dramatic action in Asian trading. INR remains under pressure after printing a new record low outright and the USD/INR is about to test the next psychological resistance at 63.00, as investors grow increasingly concerned over how the country will fare in a tighter global monetary policy environment. Officials are currently failing to stem the speculative and real pressure that their currency is under. Outright-to-date, the INR has been one of the hardest hit Emerging Market currencies with sentiment continuing to sour not wholly on the country’s weak fundamentals, but because of a lack of “credible policies to address them.” The currency has depreciated -12% this year and there is little to suggest that the collapse has bottomed out just yet. There has been little relief for the INR despite a slew of measures to correct the chronic current account deficit while simultaneously making it more expensive for offshore banks to short the currency. Will this Wednesday’s Fed remarks add to the dollar bullish pressure on the USD/INR?

In Europe, the Euro area flash PMI’s will be their main focus this week, more so after the euro-zone exited recession in 2Q. The generally stronger tone of recent data suggests that the EUR will likely remain strong in the near term. However, the prospect of a neutral to slightly dovish ECB and of reduced stimulus from the Fed could very much cap the 17-member single currency’s upside potential.

In a matter of weeks Germany will be going to the polls in the “most important election of the year”(Sept 18th). What’s rather extraordinary is virtually no debate about the major problems facing the country – exiting nuclear energy, ageing population concerns, or a debate on the euro-zone. Political pundits believe that Chancellor Merkel has pushed her party, the Christian Democrats (CDU) so close to her opposition, the Social Democrats (SPD) and Greens that the voting electorate will find them virtually “indistinguishable.”

The ECB’s head Mario Draghi pledged in July to keep ECB interest rates at record lows for an ‘extended period of time.’ The forward guidance, like Governor Carney’s at the BoE, broke with tradition of not pre-committing on policy. Earlier this month, Draghi said expectations of higher interest rates were unwarranted – a verbal warning to the market. However, it’s had little impact as the short end of the Euro curve has managed to back up +25bps since the middle of May. Along with European stocks edging lower, the price action would suggest that a market is concerned about disorderly tapering by the Fed. There is little to go on overnight with another quiet start to another week. It seems that Asian accounts are still dominating the offer side on EUR upticks. This is sure to be tested after this mornings comment from the Bundesbank. They have stated that German growth is returning to normal after a strong Q2 and that a forward guidance is not a change in the ECB’s policy. Will the market prefer being a better seller on these upticks towards last Friday’s high of 1.3380 or the months high, just above the psychological 1.3401?No matter what its seems to be the markets preference to keep things tight.

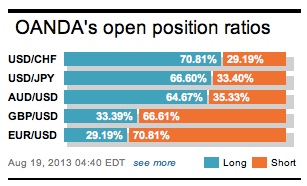

Other Links:

“To Taper Or Not To Taper” That is the Question

Dean Popplewell, Director of Currency Analysis and Research @ OANDA MarketPulseFX

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019