Bulls are knocking on the 98.25 front door once more. After being turned away around 3 times in the same number of days, USD/JPY has hit the same spot twice during early Asian trade. However, the results remained the same – 98.25 refuse to budge.

Hourly Chart

However, all is not lost, as bulls are slowly but surely gaining ground. Price has managed to form higher lows after each attempt to break down the 98.25 wall, and managed to prevent bears from getting any headway. The ability to hold above 97.50 favors the bulls greatly as it allowed for current recovery rally from 16th Apr low to remain in play. A break higher will allow acceleration towards 99.0, but ultimately bulls may need to clear the 99.0 bar in order to bring bears into submission and renew a push towards 100.0.

Stochastic readings show slightly lower peak but price action indicates that the latest attempt to break 98.25 has produced a new high. This divergence suggest that sell signals using Stochastic may not be as reliable in this case, and it also underlines the fact that current bullish pressure remains in play, despite the bear cycle that Stoch readings seem to suggest.

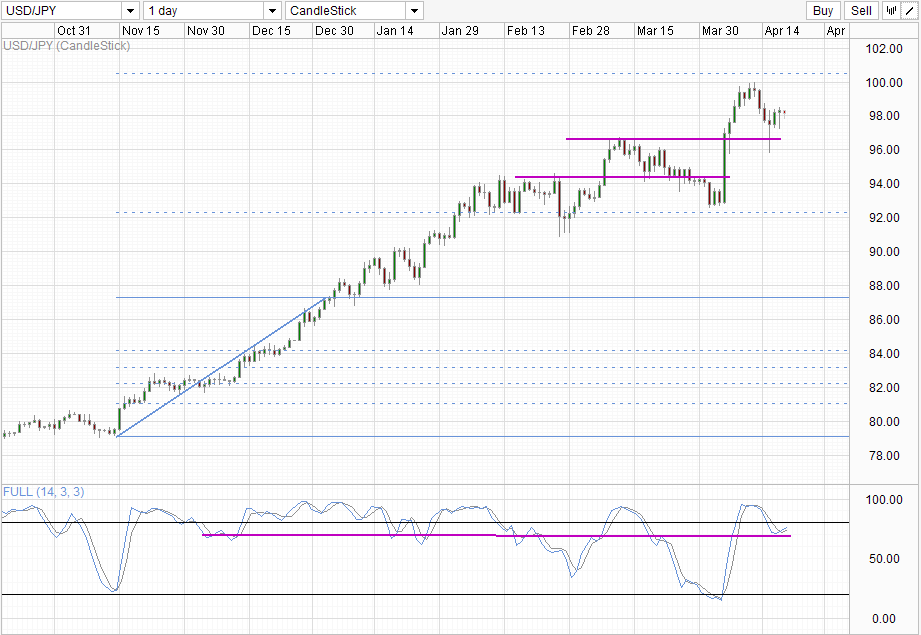

Daily Chart

Stoch readings from the daily chart is more bullish, with an interim trough already formed and readings appear to be pointing higher. Rally from last year remains intact, which suggest that a move towards the 261.8% extension is still possible as long as price does not fall below the 96.6 level (also seen in the hourly chart). Even in the event of price falling, support can be found in either of the consolidation zones marked out on the Daily Chart, with a break of 92.0 and confluence with the 161.8% Fib extension able to negate current bullish pressure.

Fundamentally, Abenomics have yet to produce tangible economic results. Beyond the weakening of Yen and Nikkei’s rally, fundamental data coming out of Japan remains weak despite Shinzo Abe’s flexing bullish rhetoric again and again. Even the latest Trade Balance statistic that came out remain negative at -¥362.4B, albeit better than previous month of -¥779.5B and expectations of -¥522.2B. Furthermore, it seems that the reason for this improving trade balance appears to be due to weakening Yen, which inflates exports that are primarily priced in USD for global trade purposes. Industrial output continue to shrink on a Y/Y basis, though M/M result is slightly better, coming in at 0.6%. But certainly we should be expecting much stronger growths since that is what Abenomics have promised.

Well, on a lighter note, Kuroda may be able to achieve his 2% inflation target sooner than expected. McDonalds in Japan has revised its 100 Yen burger to 120 Yen each. There you go, 20% inflation rate, 10 times the 2% target and many months ahead of target, which has been currently set at end of 2014 fiscal year. But more seriously, there are concerns that extreme easing measures could result in Yen going out of control. Certainly a 20% inflation rate is highly unlikely to happen, but Kuroda et al might end up getting more than what they wish for if Yen’s weakening go out of control.

Is such a situation likely? Well, it is a well known fact that BOJ failed to weaken Yen significantly in the past when the market wasn’t behind its efforts. One do not need to look far into history to find Bank of England losing out to market might in 1992. Looking at the correlation to Japanese fundamentals and Yen’s movement (or the lack thereof), it is clear that USD/JPY weakening runs more on sentiments rather than fundamentals, something that Kuroda himself acknowledged, and in fact encourage. BOJ may be grooming a beast that may well bite them back in the future, and when that happens, we could potentially see JPY weakening back towards high 100s if confidence in Japan financial system breaks.

More Links:

USD/JPY – Under Pressure Ahead of G-20 Meeting

EUR/USD – Jumps as US Numbers Disappoint

NZD/USD – Rebound higher on Higher Consumer Confidence

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Mingze Wu

Latest posts by Mingze Wu (see all)

- European Bourses Not Enjoying Bullish Winds From US Stocks - 17 April 2014

- More Aggressive Stimulus Possible Despite Premier Li’s Denial - 17 April 2014

- China March FDI -1.5% Y/Y vs +2.05% expected. First decline in more than a year. - 16 April 2014