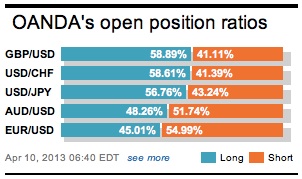

Just when you thought it was safe to go out and sell that 17-member single currency, all things turn pear-shape for the remaining ‘bear’ as the EUR takes on a new big figure level with gusto, touching $1.31 for the first time since mid of last-month. Investors to date have diligently been pairing back their anti-EUR position, ever since Governor Kuroda from the Bank of Japan announced his aggressive new easing intentions last week. Japan’s surprise policy shift has raised expectations that real money investors will continue to pull money out of Japan and go Euro asset bargain hunting. The diligent single currency bull is trying to stay ahead of the heard. The currency has not yet broken the back of the 2-month bear trend, but its close!

The significance of the Yen move is not lost on the average Japanese investor. The euphoria over Japan’s aggressive easing measure remains very much intact. The relationship between both equities and the currency value is important – a weaker Yen remains a key “wealth creation mechanism.” Governor Kuroda’s new stimulus package has certainly supported domestic equities over the past few sessions, but even with the run, the Nikkei continues to lag the US’s S&P performance over the past three-years. The market is know beginning to comprehend that to erase some of this equity gap will require USD/JPY to be trading in the 108-115 currency range – a minimum target that is very doable in the medium term.

The Yen’s dead aim tactics remain intact – with the outright currency pair honing in on the psychological 100.00 mark. It is not a matter of ‘if’ but ‘when’ for the Yen to be trading with a new three-digit handle. The currency, under Prime Minister Abe’s guidance has managed to fall almost -15% since he took office last December. The Prime Ministers large corporate supporters, and otherwise huge exporters, are in love with this currency move as they envision an end to 20-years of deflation in Japan.

The single currency trading in current ‘unfamiliar territory’ is not on the back of new global-data or even the lack of it. Since last weeks disappointing NFP report, new global fundamental headlines have been relatively sparse across the G10 divide. The EUR has been benefiting from the increasing demand for yield from the Japanese investor as Governor Kuroda’s policies are beginning to driven nominal yields down and inflation back up in the country of the ‘rising sun’, hence squeezing real yields. Also aiding the EUR is the attitude from other Central Bankers. The ECB’s loose monetary policy is everything but loose when comparing “like for like” with other policy makers agendas. The Fed, BoJ and even the BoE are more aggressive than Draghi and company. The single currency is also been supported by market perception that the BoE is more eager to provide stimulus and weaken its own currency. Mind you, the EUR’s underperformance is also driven by weak US data of late.

European financial markets remain in a positive tone after an unexpectedly good French production release this morning (+0.7% vs. -0.8%, m/m). The same cannot be said for Italian Industrial production, falling more than expected in February (-0.8%). The decline in IP from Europe’s third largest economy was led by a weakening in consumer goods and investment output. On a year-over-year basis, output has fallen -3.8% for the same-month.

The CNY rose to a record high against the mighty dollar overnight after the PBoC guided the Yuan higher despite the latest trade data showing the country swinging into a deficit last month. The country happened to record a small trade deficit of -$0.9b in March, down from a strong surplus of +$15b the previous month as imports picked up. Imports rallied +14.1%, yoy, compared to consensus of +6%, while exports rose +10%, slightly weaker than consensus for +11.7%. The market continues to expect policy makers to guide their domestic currency even higher over the coming days. The strong fix is most likely a political move after the Fitch rating agency-downgraded China’s sovereign rating. The agency happened to lower China’s long-term currency rating to A+ from AA- with a stable outlook.

With this slow burning market move, keeping investors occupied is becoming rather a challenge. The release of the FOMC’s minutes this afternoon should be of interest as investors continue to seek a “sign” for when the Fed will deviate from its current easing plan. Last Friday’s employment numbers will have certainly dampened the mood amongst US policy makers and make it even harder for Fed to scale back its QE program. The futures and forward market is trying to price in the Fed tapering back asset purchases by late September. With only +88k new jobs created last month – a five to six month deadline appears awfully tight!

It seems that many are coming to same conclusion; there is very little reason to want to sell the 17-member currency, despite such lofty heights. The EUR is likely to remain the net beneficiary of the latest BOJ policy action. Absent a sharp intensification of banking sector and sovereign stress – which has seen strong reason for capital flight out of the EUR – the underlying flow dynamics are likely to continue to keep the currency pair in demand. Now that the key resistance levels have been breached overnight (1.3100), the bias remains firmly with the EUR bull. The market is expected to stick with buying dips until clearer signals put an end to this “Bull Run.” Below 1.2925 most short term bets are off!

Other Links:

BoJ Is Standing Tall – How High USD/JPY And How Fast?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019