Euro-political instability never went away, it just lay dormant. Italy has managed to deliver to global capital markets a recipe for successful ‘political gridlock.’ A country considered as one of the strongest amongst the Euro peripheries has managed to deal a heavy blow to recent efforts to calm the Euro-periphery debt crisis. Its people have voted against austerity and reform and may be in the process of voting against the 17-member single currency unity while they are at it.

The Italian general election has yielded an inconclusive outcome, with Bersani’s PD winning the Lower Chamber by a slim margin and no clear majority in the Senate. Over the coming days Bersani will meet with Berlusconi’s PDL and Grillo’s M5S, to discuss post-election scenarios. Not unlike mainstream politics, in countries under the austerity hammer, has convinced Italian voters to reject policies pursued by sitting Prime Minister Monti.

A long recession has convinced the Italian people who have become disillusioned with mainstream politics to vote against it. The end result may give rise to the possibility of a grand coalition, which would make it even harder to make timely political decisions, or another election. Only the Italian president can dissolve parliament and call for another election. The president, who is elected by parliament, can do this once the election results are formally confirmed after March 10.

Markets dislike uncertainty. Italian bonds yields have soared and equity indexes have plummeted, as investors dump Italian debt product and flee into the safety of owning the German bund. The rejection of austerity policies by Italian voters from market darling Monti will raise doubts about the ECB’s pledge to prop up struggling Euro-economies. The ECB’s Outright Market Transactions bond-buying plan can only be activated for countries that sign up for conditions attached to an international bailout. The market will now fear Italian borrowing costs (4.72%) returning to levels last seen last summer (+6.68%).

Europe’s single currency has been on a stop-loss slugfest ever since Italian results pushed the currency back down and through 1.32 late yesterday. The next medium target is now below the 1.30 barrier. Traders have been caught leaning the wrong way since the early reporting of flattening exit polls. With investors caught firmly flatfooted has required them to dump these early optimistic trades. This market has been playing catch up ever since.

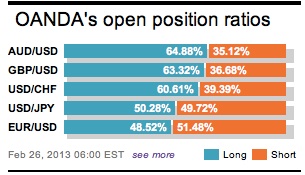

Dealers, traders and investors have always welcomed volatility. Moving asset class prices creates investment opportunities. However, you know that capital markets are up against it when investors are required to rely on Italian election piecemeal innuendo and results for participation reasons. In the end, nothing good will come of a hung Italian government for Europe. There is the fear that an uncertain outcome could lead to Greek-style paralysis in the Eurozone’s third largest economy. It is making it harder and harder for the political and economic clout to breath life back into a deflating currency. Unfavorable short Yen positions are close to being the EUR’s number one driver lower.

Can Bernanke live up to such European excitement? “Helicopter” Ben gets to testify on the Semi-annual Monetary Policy Report before the Senate Banking Committee over the next two days. Will he be correcting an implied “wrong”? The “wrong” being corrections of the reading of the recent FOMC minutes where a percentage of the market seemed to interpret somewhat hawkishly, an early end to QE3+. It was only in December that Ben and his fellow cohorts led the FOMC to more than double its outright long-term asset purchases. With US current growth data slowing below the pace required to lower the unemployment rate, there is little reason to expect any changes to the Fed’s ideology. However, there are always a few that prefer to skate too close to the edge, flapping their wings and creating more of a market nuisance than anything else.

Time is ticking. To some within the US Democratic Party the apocalypse is within striking distance. US Congress has but a few days to avert the “sequester” (the deep spending cuts) set to kick in on March 1. The cuts calls for -$1.2t slash in spending over the next 10-years. Close to -$85b of these cuts are to be delivered in the current fiscal year. All of this is an addition to the +$1.4t of spending cuts to discretionary programs announced over the past two-years. This time around it feels a tad different. While there may be a last minute deal, as there was with the fiscal cliff, it seems a bit less likely. The “sequester” is expected to shave US growth around -0.5%.

Figuratively speaking, investors should think twice before selling themselves short. Chatter involving Sterling being touted, as the investor’s new choice currency to “short” as opposed to the yen, is a tad premature. Japan, Abeconomics and a dovish BoJ governor represent a much greater shift in a particular country’s dynamics rather than a new boy wonder, Canada’s Governor Carney, being appointed at the BoE. Many are viewing yen trading close to fair value. The pound has been caught in a rating’s and a growth vortex squeeze over the past week. The market will again take its cue from UK’s growth data released tomorrow for directional guidance.

Other Links:

EUR Needs Italian Exit Polls For Clarity

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019