A lack of progress in the US budget negotiations is keeping investors on edge. The fiscal cliff in the US remains a top priority as political verbal jousting continues to create headline risk. The House Republicans made a new deficit proposal yesterday, calling for +$800b in increased tax revenue. However, this is only half of what President Obama has proposed and would take hold only through tax reform, potentially deferring any tax increases. As it becomes clearer that no agreement is likely until the very last minute, or if even then, Capital Markets should expect a fraction of this headline risk to somewhat diminish. Maybe the market is entering the domain where the political incentives are such that a resolution is more likely after going over the cliff for a short period of time?

Today’s Euro-land economic calendar is light, with the UK’s PMI for construction activity front and center. Investors will be keeping an eye on the Ecofin meeting of the Euro-finance ministers who are expected to discuss proposals for the single bank supervisor for their member states. The UK’s construction activity contracted last month after a minor pick-up in October (49.3 from 50.9), as new business slumped, consumer confidence plummeted and firms cut staff at the fastest pace in two-years. It seems that Novembers PMI print suggests that the UK construction industry has room to drop even further. Mr. Osborne, Governor King and future Governor Carney from the BoE, have a difficult task to further boost the UK construction sector that is under pressure from all sides, as UK businesses are now set for a bitter end to this year with little hope of respite in Q1.

Central Bank monetary policy announcement is the order of the day for this week. Last night, the RBA cut their overnight cash-rate target by -25bps to +3%, in line with consensus. Policy makers retained a dovish bias, however, it was ‘less’ dovish than anticipated, allowing the AUD to rally strongly into the North America open. Analysts note that there were two key changes in the following communiqué. The first is a more definitive confirmation that a peak in resource investment is approaching instead of “is likely to occur next year”, permitting the government to stimulate the economy earlier if needed. The second, while the RBA reiterated that AUD has remained high, it moved its comment on AUD to the last paragraph this month, signaling perhaps a cut is aimed at the currency more than before. Investors will get a better understanding from policy makers when the RBA’s minutes are released. Futures traders are beginning to price in another -25bp cut.

The supposed King of monetary policy announcements, Governor Carney at the BoC is again in the limelight this morning as he brings down the Bank of Canada monetary decision announcement. The market expects a boring report from the future governor of the Bank of England. The BoC is expected to maintain its overnight rate at +1% and retain its hawkish guidance. However, Analyst’s anticipate that the banks policy makers will be accommodating and downgrade their language on GDP in light of last week’s disappointing data, keeping markets cautious about pricing imminent policy tightening. It’s difficult to see the loonie aggressively changing current trading patterns. Range trading the interest and commodity sensitive currency remains the dominant course of action.

A quick trek around the globe saw Spain requesting formally the disbursement of +€39.5b of European funds to recapitalize its crippled banking sector yesterday. It’s expected that +€37b of anticipated future disbursed funds are for their four nationalized banks, while +€2.5b is for their so-called “bad bank.” The market now expects the funds to be paid to the state’s banking fund (FROB) by next week. Formalized European backing has been able to give the single currency that extra leg up, but for how long?

China and South Korea have agreed to boost the use of the Yuan and Won in bilateral trade. These agreements will certainly puts a dent in the dollars ‘reserve’ armor. Both mentioned countries are expected to begin lending trading firms their respective currencies later this month for use in settling trading deals. China currently purchases +25% of all Korean exports, while payment in either currency only accounts for +3%. Deals are mostly settled in dollars.

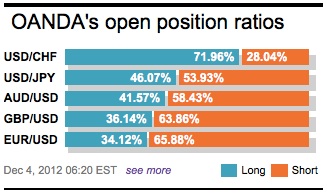

The EUR has found itself in new territory. The single currency looks to have room for further upside movement as the short positions in EUR remain significant and the recent upwind of further bets against the currency could push the EUR outright higher. The upper Bollinger prices are stalling (1.3089), but with day charts heading north a push through the band is reasonably possible. Consensus seems to have found that intraday traders are possible looking to reload and go long the single unit on reasonable dips. The trend remains with the buyer above the 1.2881 low mid-last week. Be weary that the further we go deeper into the month of December, fundamentals and technical can sometimes be easily tossed to the wayside!

Other Links:

How much stamina has the EUR got?

This article is for general information purposes only. It is not investment advice or a solution to buy or sell securities. Opinions are the authors; not necessarily that of OANDA Corporation or any of its affiliates, subsidiaries, officers or directors. Leveraged trading is high risk and not suitable for all. You could lose all of your deposited funds.

Dean Popplewell

Latest posts by Dean Popplewell (see all)

- Euro zone bond yields sink as German manufacturing slows - 24 July 2019

- How Boris Johnson Plans to Deliver Brexit in 100 Days - 24 July 2019

- Weak PMI’s Sink EUR - 24 July 2019